AB-PMJAY covers roughly 500 million people and is one of the largest public health insurance programmes in the world. A study published in BMJ Open this year is the first large-scale analysis of what it has actually delivered, four years in. Early studies have shown preliminary to negligible results, but this is one of the first studies to measure the progress after an extended period of time.

The findings are worth sitting with.

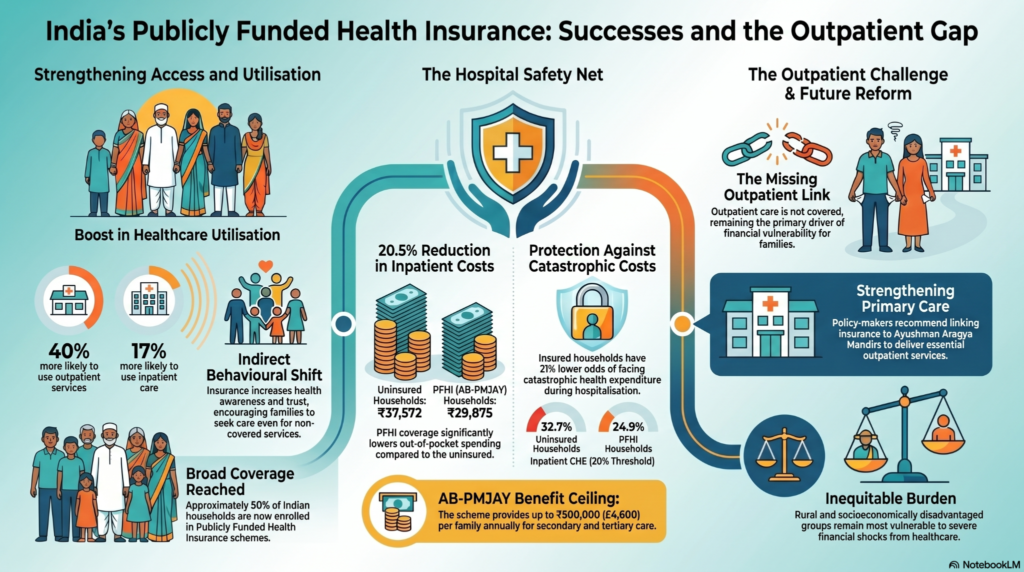

Bonu and Bhushan analysed data from over 302,000 households surveyed between July 2022 and June 2023 under the Comprehensive Annual Modular Survey. They looked at three things:

- whether insured households used more healthcare,

- whether they spent less on it,

- and whether they were protected from catastrophic expenditure – defined as health spending that exceeds a threshold of total household consumption.

On hospitalisation, the scheme performs. Households covered under PFHI spent an average of INR 29,875 on an inpatient episode, against INR 37,572 among the uninsured. The odds of facing catastrophic expenditure during hospitalisation were 21 percentage points lower for insured households.

In outpatient care, the picture is different. Insured households spent INR 1,640 on outpatient care in the past 30 days. The uninsured spent INR 1,755. The difference is not statistically meaningful. At the 10% catastrophic expenditure threshold, there was no significant protection at all for outpatient costs. AB-PMJAY does not cover outpatient care and outpatient care is where most households spend on health.

The scheme’s design draws a line at the hospital gate. Everything before that gate, the consultation, the medicines, the diagnostic test, the follow-up visit, remains entirely out-of-pocket.

The architecture of the gap

There is a finding in the study that complicates the picture further.

Insured households were 40% more likely to seek outpatient care than uninsured ones.

The authors offer several explanations. Insurance enrollment increases health awareness and trust in formal providers. Inpatient episodes generate referrals that lead to outpatient visits. Being in the scheme changes how households relate to healthcare systems generally. All of this is consistent with what health systems research would predict.

But more utilisation without financial protection means more exposure to costs. The households most enrolled in PFHI, rural, lower income, scheduled tribes, are also the households for whom a day’s treatment cost carries the most weight.

The study is careful about causality. Since it is cross-sectional, it cannot rule out that households with greater health needs are both more likely to be enrolled and more likely to seek care. But the expenditure data is direct. What households pay out-of-pocket does not change materially based on insurance status when the care they are seeking is not covered.

The Ayushman Arogya Mandirs (Health and Wellness Centres) are the government’s answer to the outpatient gap. The study recommends linking benefit packages to the HWCs and piloting outpatient coverage in select states before scale. These are directions the government has itself signalled and the infrastructure exists in some form.

In the meantime, the gap sits where it sits. Most healthcare interactions in India happen outside hospitals. That is where household financial vulnerability is highest, and where the insurance architecture currently stops.

Where CSR sits in this picture

CSR health financing in India tends to cluster around the visible and the acute. Camps, surgeries, diagnostics, equipment donations. There is a rationale for this: companies need to demonstrate impact on short timelines. But these interventions operate within the same gap the insurance data describes. They do not change the structure of the system that creates it.

Nachiket Mor, economist and member of the Lancet Commission on India’s health system, draws a distinction between what CSR typically does and what it is structurally positioned to do.

In a conversation recorded for NuSocia in November 2024, he identified two specific roles he believes CSR and the nonprofit sector can play that neither the government nor the private sector can replicate at this stage.

The first is model development for primary care.

“Primary care will need to be modernised, and will need to be operated by non-physicians,” he said. “The idea of the UK GP being in every village seems just infeasible for us.” The government has built 150,000 health and wellness centres. The models that informed that design came, in part, from CSR-funded pilots. Mor was involved in one: a non-physician-staffed clinic model called Swasth India that ran across approximately 20 clinics and two lakh population. “The government then invited us to participate in designing the health and wellness centres,” he said. “Models like ours formed the basis of this approach.”

His argument is not that CSR should deliver primary care at scale. It is that the next generation of primary care design needs to be developed somewhere and the government is not well placed to run open experiments within its own system. “It would be unethical to do so,” he said, “because it could start to disrupt the government’s ability to do its core work. It’s better to experiment outside, build something strong and viable, and then go to the government and say: we have this working.”

The model that results from that process can then move to government adoption, or to a private sector player building a managed care system that does not yet know how to deliver primary care.

The second role he identifies is sustained financing for high-need populations that do not fit neatly into either government or market-based provision.

He describes his association with The Banyan, an organisation working with homeless women with severe mental disorders. “Not a small, in India nothing is small, but a smallish population. A high need, high engagement population.” The Banyan has built the capacity to understand this population across the full life cycle, not just in acute episodes. That kind of specialised institutional knowledge does not form inside government departments. It requires long-term investment in a focused organisation.

“Some of this could be taken over eventually by the government,” he said. “But it’s possible these very high-need populations may need a combination of tax financing and CSR financing in the long run.”

CSR budgets are modest relative to total health expenditure. But they are consistent enough, Mor suggests, to sustain this kind of work, and in some cases indefinitely.

The CAMS study quantifies what households in India pay for care that insurance does not reach. The outpatient data is the clearest part of that picture. It is not a gap that AB-PMJAY was designed to address. It is one the current reform agenda has identified but not yet closed.

CSR sits in this space by default, because most health programming happens outside hospitals. The more useful question is whether it is being deployed in that space in ways that produce knowledge and models the wider system can use, or in ways that remain local and self-contained.

The evidence base for what works in primary care at low cost, non-physician delivery, and complex population management is not large in the Indian context. What exists has come largely from civil society organisations. Some of it has already shaped government policy.

There is definitely room for more of that in the CSR landscape.

Sources:

Bonu S and Bhushan I, ‘Is publicly funded health insurance associated with healthcare utilisation and financial protection in India? Evidence from a cross-sectional household survey (CAMS 2022–2023)’, BMJ Open 2026;

NuSociology conversation with Nachiket Mor, November 2024.